Roof and solar projects often land between $15,000 and $45,000+ for U.S. homes — and how you pay can matter as much as the sticker price. This guide walks through realistic home improvement financing options homeowners use in 2026, what each path costs in interest and flexibility, and red flags that signal a bad deal.

Run numbers in our solar ROI calculator and roof cost estimator first so financing discussions start from facts, not fear. Set your state in the location bar for labor-adjusted roof ranges.

Pay Cash (Or Mostly Cash)

If you have savings, paying cash (or a large down payment) usually wins on total cost. You avoid dealer fees baked into solar loans — often 15–30% of project cost — and you keep full ownership from day one, which simplifies the federal tax credit and home sale later.

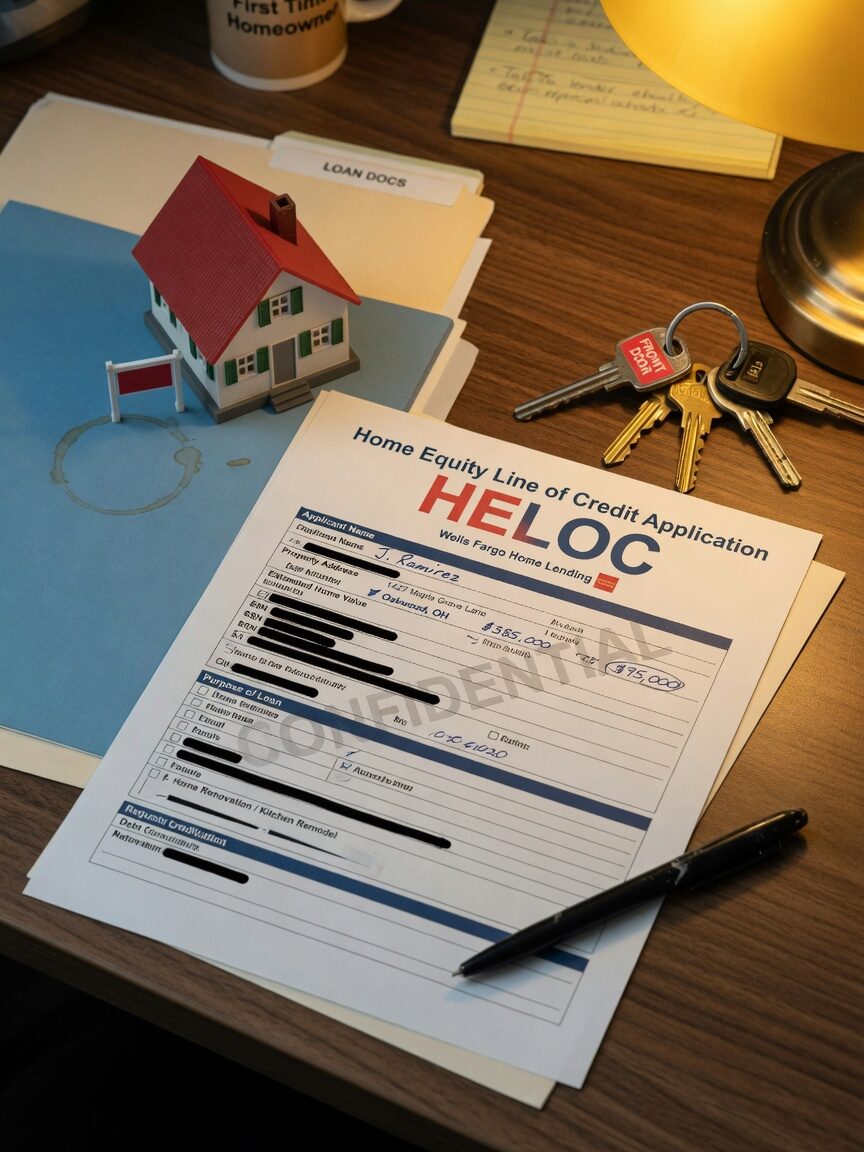

HELOC or Home Equity Loan

Many homeowners with equity use a HELOC or fixed home equity loan for roofs and solar. Rates track the broader interest market; deductibility of interest depends on current tax law and use of funds — ask your CPA. Advantages: you control the contractor, you own the equipment, and you are not tied to a solar lease. Risk: your home secures the debt; budget payments before rates adjust on variable HELOCs.

Unsecured Personal Loans

Credit unions and regional banks offer unsecured home improvement loans — often roughly 7–14% APR for qualified borrowers depending on credit and term. Compare total dollars paid over the term, not just low monthly payment marketing. Shorter terms cost less lifetime interest even if the monthly number hurts more.

Installer-Sponsored Solar Loans

Solar-specific loans are convenient but read the fine print:

- Dealer fees: A "0% down, low payment" loan may hide a 20%+ dealer fee in the principal — inflating the price you finance.

- Balloon or re-amortization: Some loans assume you pay down principal when the tax credit arrives. Miss that balloon and payments jump.

- Ownership: Confirm the loan is not structured as a lease or PPA dressed up as "loan." You want the system in your name.

Solar Leases & PPAs — Usually Not for Everyone

Leases and power-purchase agreements can make sense for narrow situations (limited tax appetite, no desire to maintain equipment). Downsides: you typically forfeit the federal ITC (the company takes it), escalator clauses raise price over time, and transfers can complicate home sales where buyers want clean title. We generally recommend ownership when you have tax liability and plan to stay 7+ years.

PACE & Property-Assessed Programs

PACE-style financing availability varies by state and municipality. Understand that assessments can transfer with the property and may affect refinancing. If someone pitches no money down tied to your tax bill, slow down and compare with a credit union quote.

Credit Cards — Emergency Only

Using cards for a full roof or array rarely makes sense unless you are in a true emergency leak scenario and can pay off a 0% promo period fast. For smaller jobs, a roof leak repair kit may buy time to finance properly.

Stack Rebates Before You Borrow

IRA HEAR and HOMES home energy rebates are not loans — they can reduce cash you need for heat pumps, wiring, and panel upgrades that often ride alongside roof and solar projects. Map eligibility in our HEAR home energy rebates guide before you size a HELOC or solar loan; point-of-sale HEAR dollars change how much principal you actually need to finance.

Solar loans sometimes assume you will apply the federal ITC as a lump-sum paydown. HEAR rebates follow different timing and trade rules — confirm with your CPA and state portal so balloon payments do not surprise you after efficiency work completes.

Questions to Ask Any Lender

Advertisement

- What is the APR, term, and total dollars paid including fees?

- Who owns the system — me or the lender — until paid off?

- What happens if I sell the home in three years?

- Is there a prepayment penalty?

- Does this loan require UCC filings on my property?

See how to vet contractors before anyone pressures you to sign financing on the first visit.

Frequently asked questions

Is a solar lease better than a loan?

Usually not if you have tax liability and plan to stay 7+ years — leases often forfeit the federal ITC to the lessor.

Can I use a HELOC for roofing?

Yes — many homeowners do; your home secures the debt, so budget for rate changes on variable HELOCs.

What is a dealer fee on solar loans?

A fee baked into principal that inflates financed cost — compare total dollars paid, not just monthly payment.

What are HEAR home energy rebates?

HEAR is a federal IRA program rolled out state by state for heat pumps, wiring, and efficiency upgrades — check our nationwide guide and your state's official portal before you borrow.

Model payments before you commit

As an Amazon Associate, Roofinghut earns from qualifying purchases at no extra cost to you. Tax and incentive details change — verify with your CPA, utility, and installer.